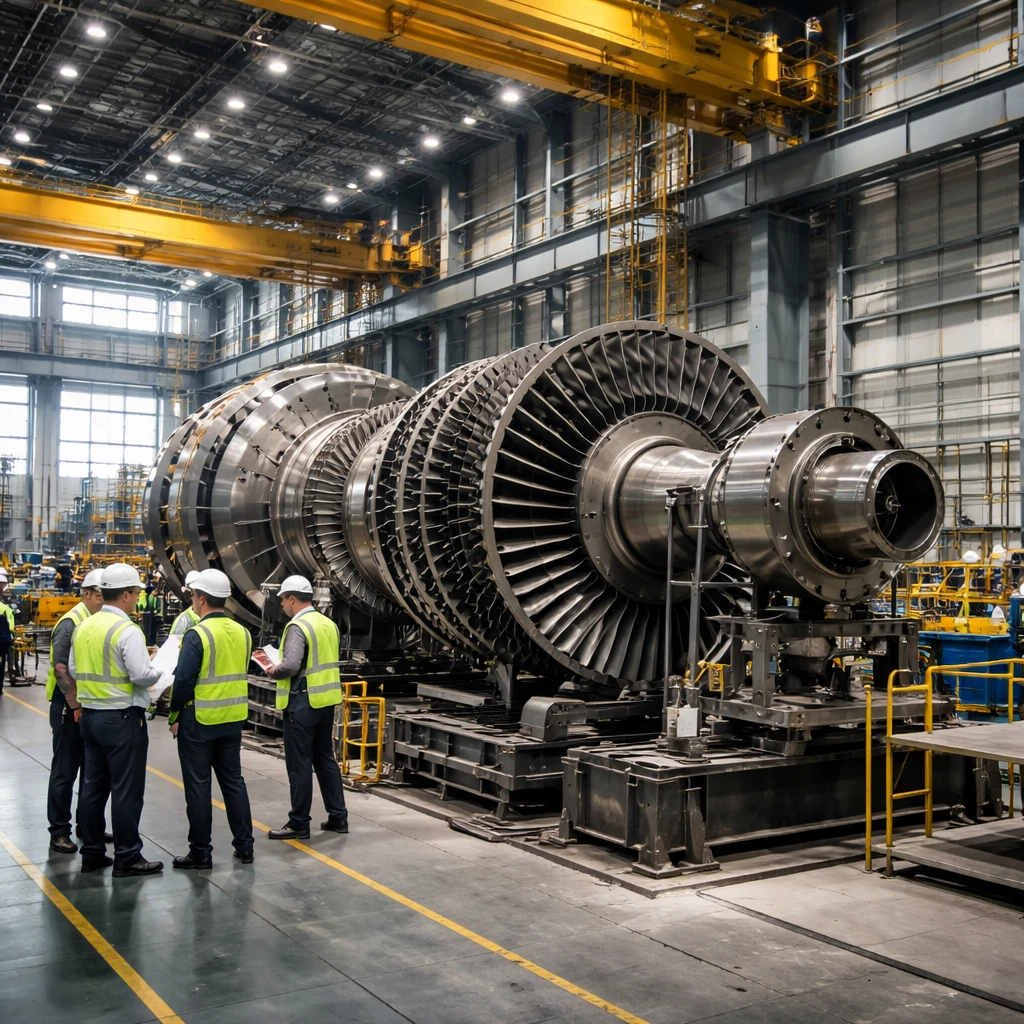

Shares of Mitsubishi Heavy Industries rose 2.4% to ¥3,652 on Monday following media reports that the company plans to double its capacity for large gas turbine manufacturing by fiscal year 2030. The report said the expansion would be financed by a capital commitment of more than ¥100 billion directed at production sites in both Japan and the United States.

Market participants tied the capacity move directly to a sharp uptick in electricity use from AI data centers. That growth in power demand has been associated with a succession of new and enlarged gas-fired power plant projects, most notably in the U.S. market, which is creating elevated demand for Mitsubishi Heavy Industries’ core turbine portfolio. Early trading saw the stock push to a session high of ¥3,774 before trimming some gains.

The expansion news arrived against a backdrop of solid corporate fundamentals. Mitsubishi Heavy Industries’ most recent full-year results showed net income up roughly 35% year-over-year. The company also reported an order backlog in excess of ¥13 trillion, a level that provides a multi-year revenue runway and supports longer-term planning for capacity increases.

Analysts have responded positively on balance. The consensus rating across the broker community is Buy, with an average 12-month price target of ¥5,323, which sits well above current trading levels. That consensus suggests investors and analysts view the announced capacity enlargement as aligned with a sustained growth trajectory for the company’s energy systems business and its defense-related operations.

For market observers, the decision to allocate over ¥100 billion to facilities in Japan and the U.S. signals a strategic bet on meeting rising near-term demand while preserving optionality across geographies. The linkage to AI-driven electricity consumption frames the capacity plan as a response to a concrete demand shift rather than a speculative bet.

While the stock reaction was positive, the price action also reflected some intraday profit-taking after an early surge. Nevertheless, the combination of improving earnings, a substantial backlog and analyst support helped sustain investor interest following the expansion announcement.

Key points:

- Mitsubishi Heavy Industries plans to double large gas turbine capacity by fiscal 2030, with more than ¥100 billion earmarked for facilities in Japan and the U.S.

- The move is tied to rising electricity demand from AI data centers and a wave of gas-fired power-plant projects, especially in the U.S., boosting demand for MHI’s turbine products.

- Company fundamentals - including a roughly 35% year-over-year rise in net income and an order backlog exceeding ¥13 trillion - reinforce investor confidence; analysts hold a consensus Buy with an average 12-month target of ¥5,323.

Risks and uncertainties:

- Execution risk around scaling manufacturing capacity in Japan and the U.S. - affects the industrial and manufacturing sectors tied to power equipment production.

- Demand concentration linked to AI data center electricity use and U.S. gas-fired power projects - if those projects slow, demand for turbines could be weaker than anticipated, impacting energy systems revenues.

- Short-term stock volatility as investors react to intraday moves - financial markets and equity investors may see price swings despite the longer-term order backlog.