Hook & thesis

Applied Digital is one of the clearest single-company plays on the ongoing AI-capex wave. The company builds and operates high-power density data centers - the kind of physical infrastructure hyperscalers and AI-specialized clouds need as model training pushes power requirements into the megawatt-per-rack range. Recent financings and lease activity have validated the strategy: Applied Digital is selling capacity to big customers under long-term contracts and expanding supply rapidly.

That said, this is not a low-risk pick. The stock trades with stretched multiples and heavy leverage, and the business is concentrated on a handful of customers. For traders who can tolerate that profile, I'm constructive on a long trade sized for an aggressive allocation with a clearly defined entry, stop and target and a 180-trading-day holding period to let capacity ramp and contracted revenue flow.

What Applied Digital does and why the market should care

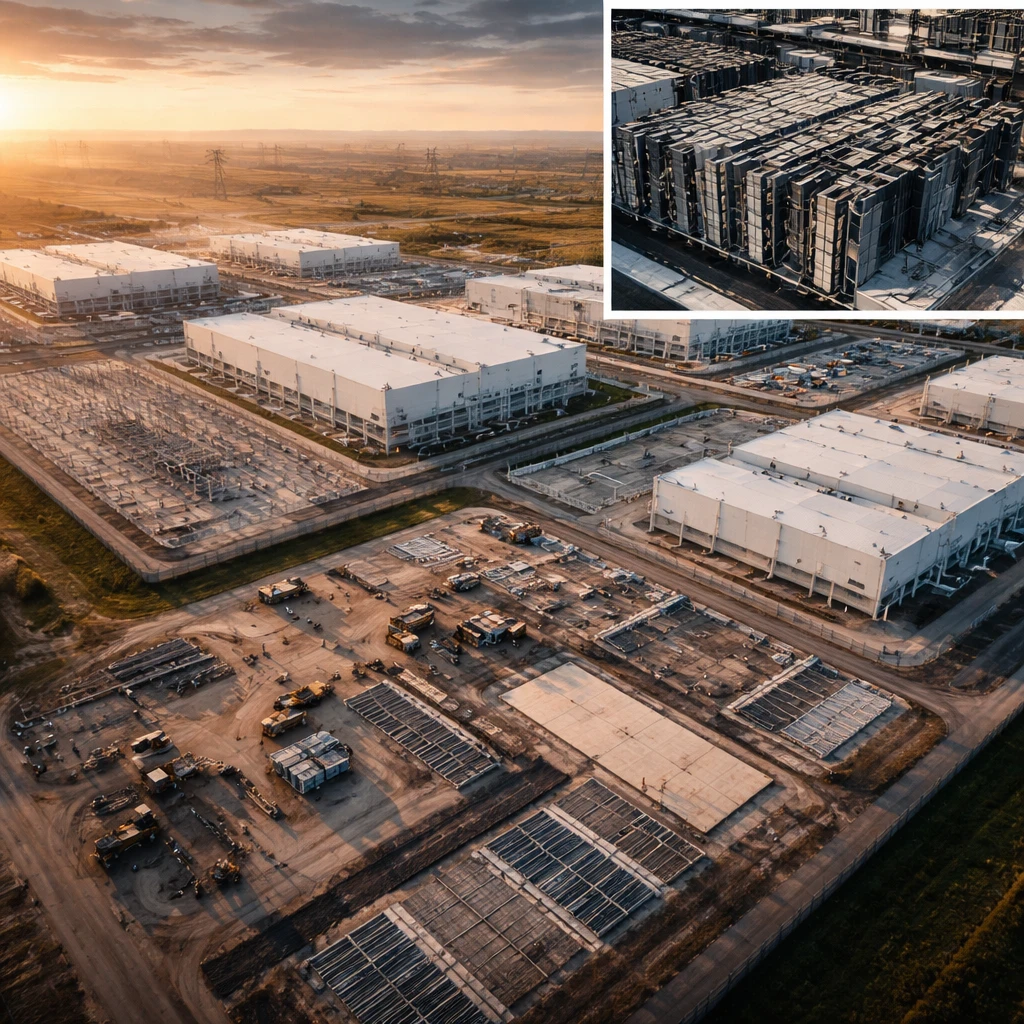

Applied Digital builds, owns and operates data centers tailored for two adjacent markets: crypto mining (energized infrastructure) and high-performance computing / AI hosting. The latter is the strategic growth engine. These facilities are engineered for high power density and specialized cooling and are leased on multi-year contracts to customers that demand scale and uptime.

The market cares because AI model training and inference are driving a structural increase in compute intensity and data-center power consumption. Physical capacity is scarce in the right geographies and with the right power profiles. Applied Digital's playbook - lock long-term contracts, raise capital to build scale fast, and monetize specialized campuses - allows it to participate directly in the AI capex boom.

Supporting numbers

Concrete metrics reinforce the narrative:

- Market capitalization sits around $7.65 billion and enterprise value at roughly $8.34 billion.

- Valuation multiples are elevated: price-to-sales near 25.7 and EV-to-sales about 29.4 - consistent with a growth story priced for perfection.

- Profitability is not yet a tailwind: trailing EPS is negative and free cash flow is negative roughly $1.81 billion, indicating continued cash burn during buildouts.

- Leverage is meaningful: a debt-to-equity ratio near 1.68 and recent financing that added about $2.15 billion of bonds, bringing total debt near $5 billion per reported items.

- Contracted pipeline is material: the company has been cited as having roughly $16 billion in contracted lease payments across its portfolio, including a notable ~$5 billion, 15-year lease tied to the Polaris Forge 2 campus.

- Customer concentration is a double-edged sword: large, long-term deals validate demand but create counterparty risk; several articles point to a high share of revenue tied to CoreWeave and other major tenants.

Valuation framing

Applied Digital is being priced like a high-growth infrastructure platform rather than a traditional REIT. A price-to-sales of ~25.7 and EV-to-sales ~29.4 reflect the market assigning a premium for contracted growth and the structural nature of AI demand. That premium is reasonable only if (1) the company executes buildouts on time and on budget, (2) its large tenants remain solvent and continue to expand, and (3) capital markets remain receptive to funding large, front-loaded build programs.

There are warning signs: negative free cash flow and an EV/EBITDA ratio that is extremely stretched. These are typical for capital-intensive roll-ups in an early growth phase, but they increase the binary nature of the outcome. If the company hits its milestones and converts contracted backlog into recognized revenue, the valuation can be justified or compressed favorably as growth accelerates. If builds stall or tenants duel on economics, the multiple will likely re-rate lower.

Technical snapshot

On the technical side, short interest has been consistently elevated with days-to-cover roughly 4-5 days in recent settlement periods and high short volume on multiple sessions. Momentum indicators show a neutral-to-constructive setup: the 10-day SMA is below current price and MACD is signaling bullish momentum. That setup favors a timed entry with a tight stop to manage the downside volatility that comes with high short activity.

Catalysts to watch (2-5)

- Operational ramps at Polaris Forge 2: the commencement of commercial service or tenant power-ups will turn contracted pipeline into revenue and materially de-risk the story.

- Leasing starts and expansion announcements from anchor tenants (Oracle, CoreWeave, etc.). New or expanded long-term leases would validate pricing power and utilization assumptions.

- Balance-sheet maneuvers: successful debt management, refinancing, or asset monetizations that lower leverage would be positive.

- AI-capex momentum: broader AI capex easing/refinancing in the market and continued commitments from hyperscalers would underpin long-term demand.

Trade plan (explicit entry / stop / target and horizon)

Entry: buy at $27.35.

Stop loss: $22.00.

Target: $40.00.

Risk level: high.

Horizon: long term (180 trading days) - plan to hold through the next major construction/commissioning cycle and several tenant power-ups. The primary driver for the timeframe is that data-center projects take quarters to bring online and leases convert to revenue only after commissioning; 180 trading days gives time for at least one meaningful operational milestone or financing/lease event to occur.

Sizing: treat this idea as an aggressive growth allocation only – the combination of elevated leverage, negative free cash flow and customer concentration argues for limited position sizing within a diversified portfolio.

Counters and risks - balanced view

Below I list key risks and a direct counterargument to the bullish thesis.

- Customer concentration and counterparty risk: a very large share of future contracted revenue is dependent on one or two customers. If CoreWeave or another anchor faces liquidity stress or renegotiates terms, Applied Digital's revenue and cash flow profile could be materially impaired.

- High leverage and negative free cash flow: the company recently added roughly $2.15 billion in bonds, pushing total debt toward $5 billion. Free cash flow was negative around $1.81 billion, increasing refinancing and covenant risk in a stressed market.

- Valuation vulnerability: multiples like price-to-sales near 25.7 leave little room for execution missteps; any delay in lease commencements or margin compression could produce a sharp multiple contraction.

- Execution and construction risk: large data-center builds routinely face permitting, supply chain and labor challenges. Delays push out revenue recognition and increase cash burn.

- Concentration on AI customers tied to a narrow upstream ecosystem: several customers depend on a limited set of AI software/hardware suppliers; if those end markets pause spending, the demand tap can slow quickly.

- Market sentiment / technical risk: heavy short interest and large short volumes can accelerate downside moves during negative headlines.

Counterargument to the bullish case: valuations are priced for perfection. If AI capex cools or if anchor tenants scale more slowly than expected, Applied Digital's stretched multiples and leverage could combine to produce meaningful downside. In that scenario, capital raises would be dilutive and the share price could trade materially lower.

Why I still prefer a tactical long

Two factors tilt the risk/reward toward a tactical long for the aggressive trader. First, the company has locked long dated revenue under large leases (including a multi-billion dollar arrangement tied to Polaris Forge), which reduces pure demand risk. Second, the market's narrative around AI infrastructure continues to attract capital and customers; when a company can combine locked-in demand with fast scale, the revenue trajectory can change quickly and justify a premium multiple in short order.

What would change my mind

- Reversal: if a major anchor tenant publicly reduces its contracted load or files for bankruptcy, I would exit and re-evaluate the thesis.

- Debt deterioration: if new filings or disclosures suggest the company cannot service near-term maturities without highly dilutive equity issuance, that would push me to a negative view.

- Operational delays: missed commissioning dates for Polaris Forge 2 or other key builds without visible remediation plans would erode conviction.

Conclusion

Applied Digital is a high-upside, high-risk way to play the AI-capex cycle. The company's access to contracted, long-duration revenue and its ability to rapidly scale purpose-built capacity are compelling if execution and counterparty risks are managed. For traders who accept those risks, the defined-entry long at $27.35 with a $22 stop and $40 target over 180 trading days provides a structured way to participate without turning this into a full conviction, buy-and-hold core position.

| Metric | Value |

|---|---|

| Market cap | $7.65B |

| Enterprise value | $8.34B |

| Price-to-sales | 25.7 |

| EV-to-sales | 29.4 |

| Free cash flow | -$1.81B |

| Debt-to-equity | 1.68 |

| Contracted pipeline (reported) | ~$16B |

Trade idea summary: long APLD at $27.35, stop $22.00, target $40.00, horizon long term (180 trading days). Position size for aggressive investors only.